UK savers need to save seven times their annual household income by aged 68, compared to an average of 10 times in other parts of the world.

UK savers need to save less of their household income than those in the US, Germany, Canada, and Hong Kong and a comparable amount to those in Japan for retirement. According to calculations from Fidelity International’s global retirement savings guidelines1, UK savers need to put away 7 times their annual household income by age 68, compared to an average of 10 times in other parts of the world to maintain the lifestyle they had pre-retirement.

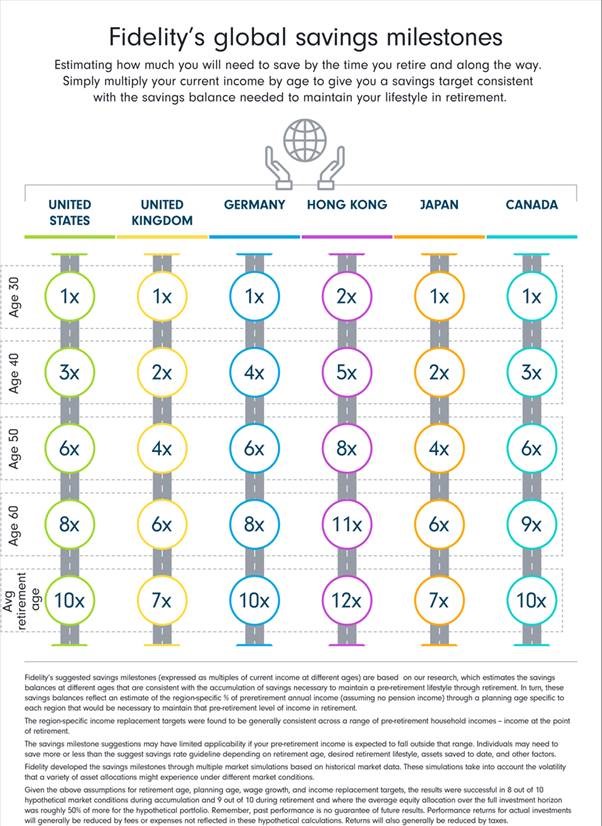

What are Fidelity’s global retirement savings guidelines?

The brand new global retirement savings guidelines from Fidelity, which are an industry-first, have been used to generate a global standard for keeping retirement savings on track. Designed to provide savers with a set of simple “rules of thumb”, accessed by an interactive tool, the global guidelines help address the two most common retirement-related questions from those saving for retirement: “How much do I need to save for retirement?” and “Am I on track to save enough?”

Based on the input of two metrics that everyone knows – their age and their salary – the guidelines provide savers with a straightforward suggestion on what percentage of their annual household income they should be saving (yearly savings rate) and what multiple of their annual household income they should have saved at each stage of their life (savings milestone) .

In addition, the guidelines also provide an indication of the amount of income they would need to replace to maintain their lifestyle at retirement (income replacement rate) and how much a household can afford to take from their retirement savings each year to ensure that it lasts through retirement (probable sustainable withdrawal rate).

The results and what it means for UK savers:

Global analysis from the Fidelity retirement savings guidelines identified that the savings milestone for the UK is one of the lowest in the world needed to maintain people’s current lifestyle in retirement – just seven times their annual household income saved by retirement.

Brits should aim to save a pension pot equal to 1x their annual household income by the time they are 30, two times by the time they are 40, increasing to seven times by the time their state pension kicks in at 68.

For those in the UK, to reach that seven times milestone means saving 13 per cent a year from the ages of 252 to 68. Auto-enrolment means that from April 2019, for those in full time employment, employers will contribute at least 3 per cent, and employees will also be contributing 5 per cent of their salary pre-tax from April 2019. This means UK savers only need to save an additional 5 per cent to reach their 13 per cent savings rate.

By following these guidelines, and saving 13 per cent a year and reaching that 7 times savings milestone, this should help households in the UK to replace 35 per cent of their pre-retirement income, with the rest being supplemented by any state pension provisions, to reach the expected total income replacement rate of 55 – 85 per cent.3

Maike Currie, Investment Director at Fidelity International, comments: “While UK savers need to save less than other countries, there is still a lot more that could be done to educate and prepare the population to save for their retirement. Auto-enrolment has had a real impact, with 73 per cent4 of employees now contributing to a UK pension, and employers have a significant role to play in engaging their workforce. However, the onus is still on individuals to make sure they’re saving enough. This is why we have developed these simple rules of thumb to help people to achieve their long term savings goals with a little bit of financial forward planning.

“To make this easier, Fidelity has created a set of tool to simplify the savings journey, and help people understand what milestones they need to reach along the way.

“Ultimately what the saving goal is doesn’t matter; what does matter is that there is a way of getting there if the right plan is in place. At whatever age someone starts on this journey, a focus on the goals ahead is vital. Missing a milestone is not the end of the world, and can be overcome through planning and saving – the best first step is to start.”